在众多膜产品及其各种应用领域中,尤以MBR(膜生物反应器)应用在市政污水处理领域被业内人士广泛认可。自2000年起,由于膜价格出现了45%的大幅下落,并且MBR膜组器可以放置在土地面积局促的城市污水处理厂和工业废水处理设施间,MBR在全球污水处理市场的吸引力不断增强。

据Bluefield Research公司发布的新报告称,在全球已装机的420万m3/d的大型MBR系统(Bluefield将大型MBR系统定义为处理能力≥3万m3/d的系统)中,包括GE、碧水源在内的美国和中国MBR系统供应商供应了该市场超过74%的份额。其中碧水源已完成数千项污水资源化工程,总规模近1000万m3/d(见图),未来碧水源还会以低成本、核心膜技术在国际市场上继续扩大国际市场占有率。

市政污水处理将继续成为大型MBR系统的主要市场。同时,石油化工、食品和饮料以及其他行业的高有机负荷废水将为MBR进一步提供全新的市场机遇。未来,污水排放标准会越来越严格,而经MBR系统处理后的水质明显高于传统污水处理系统的出水水质,因此污水处理将更多地采用MBR工艺技术。

---.jpg")

主要MBR系统供应商的市场份额

Bluefield Research Strengthens Management Team– Keith Hays joins as VP

BOSTON, US— 3 February 2014— Bluefield Research is pleased to announce the addition of Keith Hays to its management as Vice President and Managing Director, EMEA. Keith is a seasoned market insight professional with over 15 years’ experience in the telecoms and energy sectors as a management consultant and industry analyst.

Prior to joining Bluefield, Keith spent seven years as Managing Director, Europe for Emerging Energy Research (EER) where he built out the company´s wind energy practice and European research before the firm was acquired by IHS Inc. in 2010. Since 2010, Keith served as Senior Director of renewable energy research at IHS where he lead integration of EER content into the IHS organization, directed renewable energy consulting projects, and supported the firm´s European power market insight services.

At Bluefield Research, Keith will manage the company´s European operations and lead the firm´s push into private water markets.

“We are delighted to have Keith on board. His proven leadership in building out insight services and international expertise will be key to help clients understand the complexities of a water industry on the cusp of major changes,” said Reese Tisdale, President and CEO of Bluefield Research.

Keith will build up Bluefield´s operations in Barcelona, Spain where he has lived for the past 15 years, providing Bluefield Research an increasingly global presence.

“Joining Bluefield is an exciting opportunity to make a lasting impact on investor strategies in a most strategic sector,” said Hays, “I look forward to delivering research solutions to the many challenges that lie ahead in water”.

###

U.S. and Chinese Suppliers Lead Global Membrane Bioreactor Market, According to Bluefield Research

Can U.S. suppliers keep emerging Chinese competition at bay?

BOSTON, US— 13 January 2014— The global membrane bioreactor (MBR) market is set to rebound, with U.S. and Chinese suppliers poised to win the lion’s share of contracts according to Boston-based water market analysts Bluefield Research. Water and wastewater markets in general have been set back by the global economy, but the MBR market is regaining momentum with over 1.6 million cubic meters per day (m3/d) of large-scale MBR capacity in planning.

“Increasingly stringent water discharge limits, especially those protecting sensitive waterways, are prompting a move to MBR technology,” says Bluefield Research analyst Erin Bonney. “MBR systems produce higher quality effluent than conventional wastewater treatment systems.”

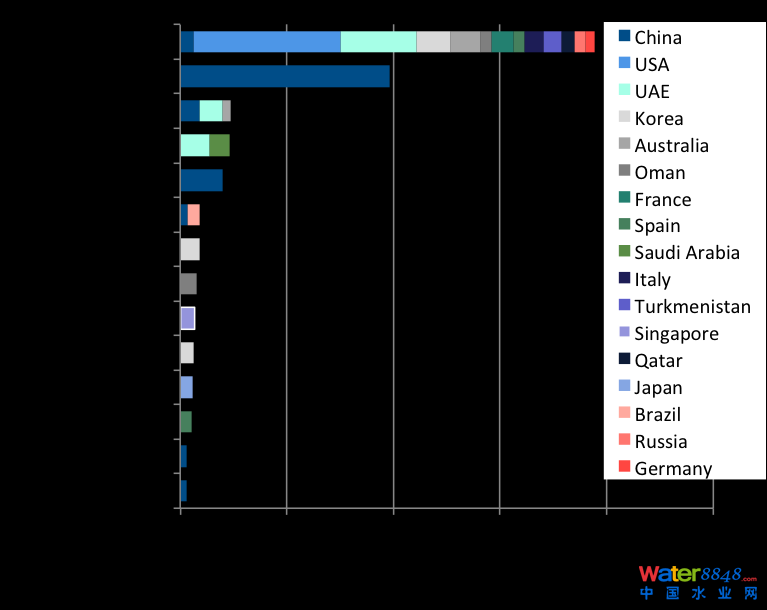

Of the 4.2 million m3/d of large-scale MBR capacity installed worldwide, U.S. and Chinese system suppliers– GE Water, Beijing Origin Water, Koch Membrane Systems, Beijing E&E, and Tianjin Motimo– have supplied over 74 percent of the market, according to a new report from Bluefield Research. Bluefield defines large-scale MBR systems as those with a capacity greater than or equal to 30,000 m3/d.

GE Water is the market leader in large-scale MBR systems with nearly a 47 percent global market share. GE Water has strong supply references in the U.S., U.A.E, South Korea, Australia, and France, but has supplied just 61,000 m3/d to the booming Chinese market.

China, spurred by 2008 Olympics build-out and continued urbanization, is the world’s largest MBR wastewater market with over 1.4 million m3/d installed to date and has 730,000 m3/d of additional capacity in the planning stages. Chinese suppliers such as Beijing Origin Water have emerged as the chief threat to GE Water’s global MBR position.

MBR System Supplier Installations by Country

Source: Global Membrane Bioreactor Market: An Emerging Competitive Landscape

Since 2000, MBR has found traction in the global wastewater treatment market thanks in large part to a 45 percent decline in membrane prices and MBR’s modular design, which can be deployed at space-constrained urban and industrial wastewater facilities. This positive outlook for the MBR industry has sparked vertical integration along the technology’s supply chain, enabling companies to capture greater economies.

“The municipal market will continue to be the primary user of large-scale MBR systems,” says Bluefield’s Bonney, “but high organic loads and waste volumes in petrochemicals, and other industries such as food & beverage and dairy, present further greenfield opportunities.”

Bluefield’s new report, Global Membrane Bioreactor Market: An Emerging Competitive Landscape, is part of the Advanced Water Treatment & Desalination Insight Service, and is the first report of its kind to provide competitive analysis on:

- MBR membrane supplier market share

- MBR system supplier market share

- Consolidation and supply-chain positioning

- Project cost trends.

- Regulatory environments affecting the technology’s deployment

- Analysis on the technology’s 1.6 million m3/d global pipeline

Click here for more information on this report.

###

Private Ownership Sparks New Phase of Global Desalination Growth

Private ownership is expected to account for 51 percent of large-scale pipeline development, unlocking greenfield opportunities for companies across the desalination value chain.

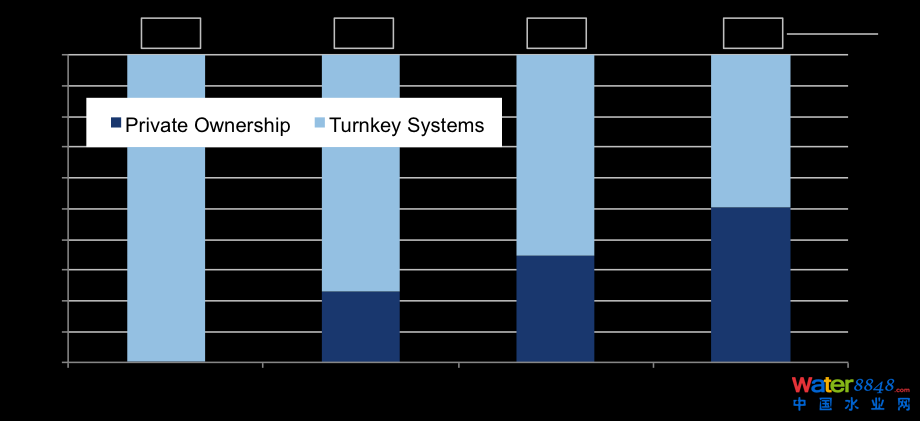

BOSTON, US— 17 December 2013— The global desalination sector is transitioning into a new phase defined by increased private sector ownership and proliferating greenfield opportunities in new markets and geographies, according to a new report from Bluefield Research. Nearly 8 million m3 per day of privately-owned desalination capacity have been installed globally since 2009, representing 35 percent of total additions during that period. Of the 25 million m3 per day of large-scale desalination projects currently planned or under construction, Bluefield estimates that 51 percent will end up under private ownership.

Global Share of Privately Owned Desalination by Year

Source: Global Desalination Market Trends & Ownership Strategies 2014-2018

Indicative of this shifting landscape, a burgeoning group of over 100 private players are expanding their ownership footprints to encompass new geographies– sub-Saharan Africa, Asia, Latin America. At the forefront are a group of pure play water companies, such as Hyflux, IDE Technologies, Mekorot, Aqualyng, Seven Seas Water, Consolidated Water, and Poseidon Resources.

“Over the next five years, desalination strategies will undergo a major transformation,” said Reese Tisdale, President of Bluefield Research. ”The status quo of relying on new-build desalination from publically-owned utilities in the Middle East will not sustain all the EPC firms and component suppliers active in today’s desalination market; as a result companies are hunting for greenfield opportunities in new markets and industries to supply.”

As part of the report’s outlook, Tisdale noted that these pure-play water companies, which possess the core competencies to build and operate desalination systems, are parlaying their expertise into greater ownership positions globally. Pure-plays are creating economies of scale across the value chain, and their desalination systems, in some cases, are producing water at

US$0.50–US$0.60 per m3 produced, some of the lowest costs globally. This is forcing established engineering, procurement, and construction (EPC) firms such as Abengoa, Acciona Water, Cadagua, Malakoff, Suez, and Veolia to reshape their strategies.

Geographically, the Middle East remains the desalination sector’s epicenter, representing 64 percent of total installed capacity since 1980. However, the past ten years have seen desalination technology deployment expand to more than 65 countries and across a mix of industry verticals, including agriculture, mining, power generation, and oil & gas. Further, new markets including China and India are in their infancy with desalination targets in place. China is less than 30 percent toward reaching its 3 million m3 per day target by 2020.

Global Desalination Market Trends & Ownership Strategies, 2014-2018 is the first desalination report released by Bluefield Research, a new market insight firm tracking greenfield opportunities in the burgeoning but complicated water sector. The 160-page report is aimed at guiding decision-makers with an in-depth analysis of the rapidly-changing desalination landscape, including key policy drivers, water supply and demand trends, technology shifts, and developing trends in project ownership. The report highlights greenfield opportunities and profiles the competitive strategies of 65 desalination project owners.

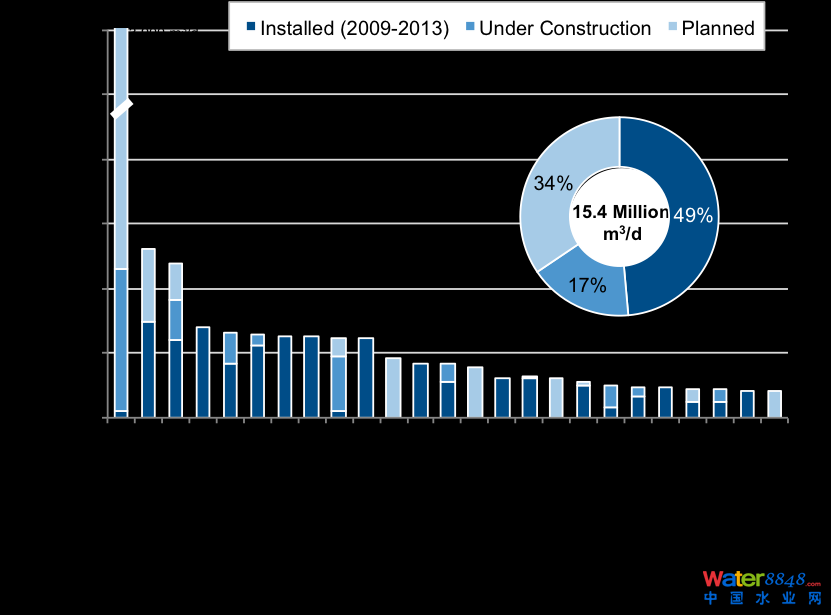

Top 25 Owner Ranking: Net Installed (2009−2013) + Under Construction + Planned to 2018

Source: Global Desalination Market Trends & Ownership Strategies 2014-2018

In addition to the role that private water is playing in today’s desal market, Tisdale noted that Bluefield Research is tracking emerging trends in industrial water risk. Demonstrated by a spate of recent activity in water-stressed industries such as mining, power, and oil & gas, Bluefield anticipates companies such as BHP Billiton, Rio Tinto, Total SA, Eskom, and AES Gener to broaden their desalination footprints. In recent months, AES Gener has gone so far as to move into water supply beyond its own needs, representing a shift in its strategy and an indicator of new opportunities in key markets.

“More than ever, industrials are under pressure to secure alternative water sources and this is a positive sign for suppliers. Industrial systems are frequently absent the typical bureaucracy and politics of municipal water and offer higher margins,” added Tisdale. “In markets like Chile, China, India, and South Africa, we’re seeing more large-scale desalination built for the exclusive use of industry. As water stressed emerging markets continue to develop their economies via power generation build-out, oil & gas exploration, and, in some cases, mining, we expect that development to create robust demand for desalination.”